This article breaks down the key differences to help you make an informed decision.

What is Car Leasing?

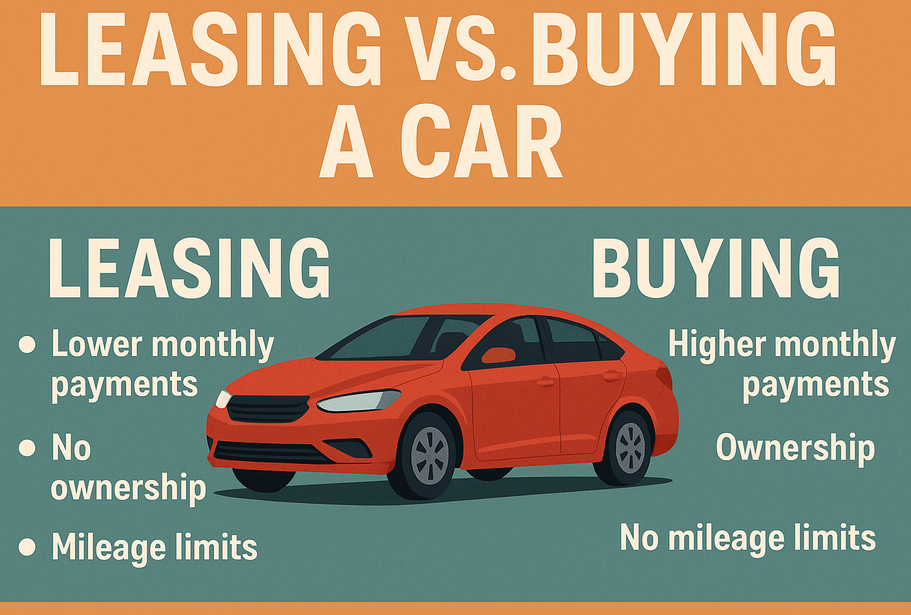

Leasing a car is essentially a long-term rental. Instead of purchasing the vehicle outright, you pay to use it for a set period - typically 24 to 48 months. At the end of the lease, you return the car or, in some cases, buy it for a predetermined price known as the residual value.

Monthly payments on a lease are generally lower than those of a car loan because you're only paying for the depreciation - the estimated value the car loses during the lease term - plus fees and interest.

However, leasing comes with restrictions, most notably on mileage. Typical leases allow 10,000 to 15,000 miles per year, and exceeding that can lead to hefty charges.

What Does It Mean to Buy?

Buying a car, whether with cash or through a loan, means you’re working toward ownership. Though monthly payments are usually higher than leasing, each payment builds equity in a vehicle you eventually own outright.

Buying is often the better long-term financial decision. Once the loan is paid off, your cost of ownership drops significantly. There are also no mileage restrictions, and you can customize or sell the car whenever you want.

Should You Buy the Car After Leasing?

At the end of a lease, you may have the option to buy the vehicle at the residual value. This can be a smart move - but only if the price makes sense.

When it’s a good idea:

- The car’s market value is higher than the residual value.

- You’ve exceeded mileage limits or caused more wear and tear than expected - buying the car may be cheaper than paying penalties.

- You like the car, and it’s in great shape.

- You know the car’s full history and would rather keep it than start over.

When to walk away:

- The residual value is more than the car’s market value - you’d be overpaying.

- You’d prefer a newer model with better features.

- You can find a better deal on a similar used car elsewhere.

Before deciding, check trusted valuation sources like Kelley Blue Book or Edmunds to compare the buyout price to the current market.

Who Should Lease?

Leasing can be ideal if you:

- Want a new car every few years

- Drive a predictable number of miles

- Prefer lower monthly payments

- Want to avoid major repair costs

- Don’t plan to modify or keep the vehicle long-term

Who Should Buy?

Buying is usually better if you:

- Want to own your vehicle outright

- Drive more than 15,000 miles a year

- Prefer long-term savings

- Plan to keep the car for many years

- Like to customize or modify your vehicle

Final Thoughts

Leasing and buying both have a place in the financial toolbox. Leasing offers flexibility and lower upfront costs, while buying delivers long-term value and freedom.

The key is to evaluate your budget, driving habits, and ownership goals. And if your lease ends with the option to buy, compare the residual value to the market value before making your move.

Smart car ownership starts with informed choices - and whether you lease or buy, understanding the trade-offs is the first step to driving with confidence.